Analysis And Portfolio Approach Cryptocurrency isn’t going anywhere. You can ignore it – or embrace it as part of a balanced investment portfolio.

https://www.moneygeek.com/investing/crypto/cryptocurrency-or-stocks/#expert=david-dubofsky-phd-cfa

To help investors make informed decisions about how much cryptocurrency belongs in their portfolio, MoneyGeek constructed its own value-weighted cryptocurrency index and analyzed the last seven years of cryptocurrency returns. We compared these returns to the well-known S&P 500 stock index, as well as a bond index.

Our analysis found that both stocks and cryptocurrencies have the potential for significant returns and losses in portfolio value. If your investment horizon and risk tolerance are suitable for these investments, our analysis pointed to the benefits of investing more in stocks than cryptocurrency. However, it also found that holding a small proportion of cryptocurrency investments can also be useful.

KEY FINDINGS:

- $1,000 invested in cryptocurrency grew to $27,000 over five years. From 2016 to 2021, that’s a compound annual growth rate of 94%.

- The S&P 500 outperformed the cryptocurrency index in 2021. From 2013 to 2022, cryptocurrency was four times more volatile than the S&P 500 over the same period and 26 times more volatile than bonds.

- After an initial period of lower correlation between assets, cryptocurrency and stocks have become more correlated through 2021 into the start of 2022, suggesting that cryptocurrencies may not be viable as a store of value.

- Incorporating cryptocurrency as a small percentage (3%) into a moderately aggressive long-term portfolio of 70/30 stocks/bonds from 2017 to 2021 would have led to 42% higher investment returns. This comes at the price of 18% higher portfolio volatility.

Does Cryptocurrency Belong in My Portfolio?

Whether investing in cryptocurrency is a good idea or a bad one depends on your risk tolerance. However, the consensus at MoneyGeek is that cryptocurrency will be around for the long run, and it’s an important new asset class.

The massive volatility of cryptocurrency assets indicates that it’s advisable not to make it a significant portion of your portfolio. That is, aim for 5% or less, not your entire retirement portfolio.

Incorporating a small proportion of cryptocurrency into your portfolio would have increased overall returns at a smaller increase in overall risk over the past five years. In our analysis of historical returns over the past five years for the hypothetical 70/30 stock/bond portfolio, we found that investing 3% of your portfolio in cryptocurrency instead of stocks for a 3/67/30 portfolio saw overall returns increase by 42%.

However, keep in mind that cryptocurrency does increase a portfolio’s overall volatility; with our 3/67/30 approach, overall portfolio volatility rises by 18%. It’s also important to consider that cryptocurrency’s long-term return and behavior are relatively unknown compared to bonds and stocks, which have been around for hundreds of years. Arguably, as more assets flow into cryptocurrency, rates of return should decline at the benefit of lower volatility.

Cryptocurrency: Big Gains for Significant Risk

While cryptocurrency has been around since 2009 — longer than it has been well-known in the public consciousness — it’s still in its infancy compared to other investment vehicles. For a while, no financial advisor who wanted to be taken seriously would recommend putting any money into cryptocurrencies. The $1.9 trillion cryptocurrency market has made many reconsider its place in a balanced investment profile in recent years.

Ever since investors began putting their money into cryptocurrency, they’ve reported dizzying gains and losses. In the five years from 2017 to the end of 2021, MoneyGeek’s cryptocurrency value-weighted index of coins increased 27 times for a 94% annual return.

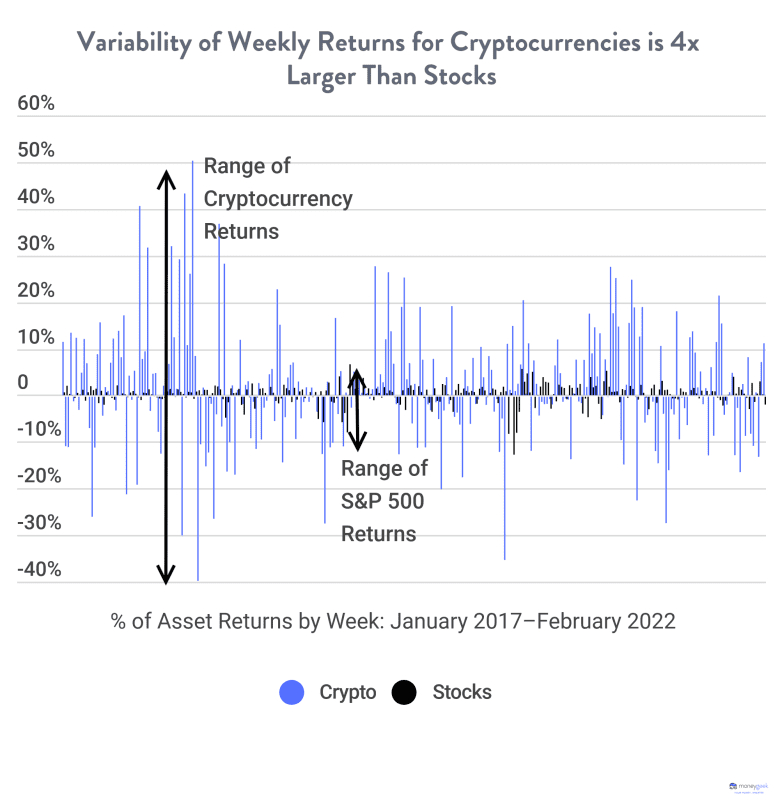

Along with breathless climbs, there have been harrowing drops in value. The worst week of cryptocurrency returns from 2017 to the end of 2021 was a stomach-churning loss of 39.5%. Most recently, Cryptocurrencies lost 14% of their value in early 2022.

Cryptocurrencies Had Weekly Volatility Four Times Larger than Stocks

A standard measure of risk is volatility, or how much returns fluctuate over time. High volatility measurements mean higher highs and lower lows, while lower volatility means more level returns. Typically, steady returns have a lower potential for significant gains as investors are often willing to give up high potential returns for increased stability. Since 2013, cryptocurrencies have had weekly volatility four times higher than stocks and 26 times higher than bonds.

For assets as volatile as cryptocurrency, it’s essential to limit your overall exposure. This way, a gain in the asset improves your portfolio, and a catastrophic loss doesn’t jeopardize it.

Generally, it’s also advisable to limit volatile investments to situations where you are investing for the long term. The logic here is that if there’s a sudden loss in portfolio value that you’ll need in the near future (think five years or less, some say 10 years), your portfolio might not ever recover from the loss.

Cryptocurrency vs. Stocks

Cryptocurrencies first came about in 2009 with the advent of Bitcoin. Comparatively, the first stock exchange was formed in 1611 in Amsterdam; in the U.S., the Philadelphia Stock Exchange was founded in 1790. With stock exchanges in the U.S. almost as old as the nation itself, there’s been plenty of time to build up systems and regulations to protect investors and put in safeguards to ensure a well-functioning market.

Splashy headlines of illegal activity, such as hackers making off with $320 million of assets, contribute to cryptocurrency risks. Aside from defrauding individuals, these events can damage investor confidence, causing other investors to curtail further investment in the assets. A famous early hack in 2011 dropped the value of Bitcoin by 94%.

However, fraud as a percentage of total transactions has decreased over time and is estimated to be 0.15% of total crypto value transacted, a small overall percentage. The same authorities regulate cryptocurrencies and the stock market. Today, cryptocurrencies are already worth a massive $1.9 trillion, indicating investor acceptance and comfort with the space. Arguably, some of the most significant asset gains are behind cryptocurrency from its earliest days, with the trade-off being more legitimacy, investor confidence and safeguards.

View the comparison chart below to explore differences between cryptocurrency and stock returns, market size, risk measures and regulation.

STOCK VS. CRYPTOCURRENCY: KEY DIFFERENCES

|

Cryptocurrency

|

Stocks

|

|

|---|---|---|

|

5-Year Annualized |

94.4% |

15.7% |

|

Market Cap |

$1.9 trillion |

$40 Trillion |

|

Weekly Volatility |

12.3% |

2.0% |

|

Biggest Single |

-39.50% |

-14.98% |

|

Regulation |

|

|

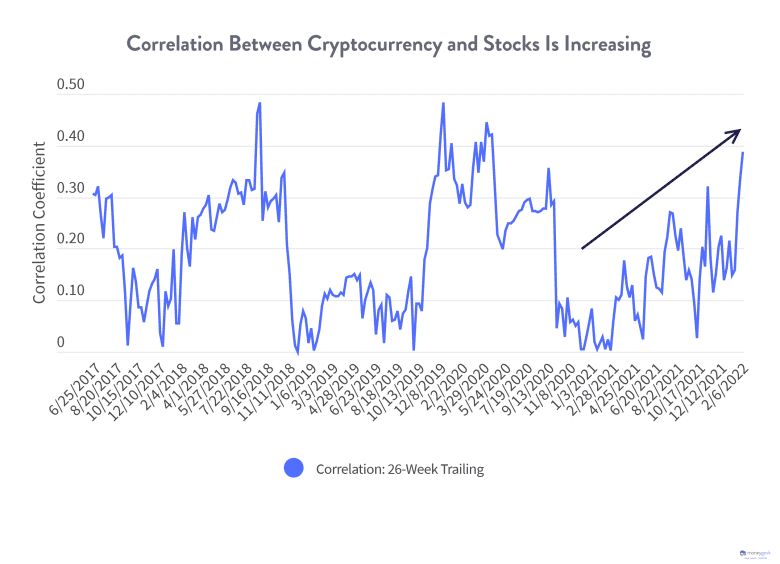

Analysis Shows Increasing Correlation Between Cryptocurrency & Stocks

In 2018, the National Bureau of Economic Research published a paper, “Risks and Returns of Cryptocurrency.” The authors concluded that the risk-return dynamics of cryptocurrencies (Bitcoin, Ripple, and Ethereum) were distinct from those of stocks, currencies, and precious metals. Essentially, they found that the change in the value of an asset like stocks didn’t mirror the changes of value of cryptocurrencies and vice versa.

“Cryptocurrencies,” the authors added, “have no exposure to most common stock market and macroeconomic factors.”

This is an important statement for investors as they think about their overall investment portfolio strategy. If an asset’s changes in value are moving with another investment, these two assets don’t offer investors protection in the event of a downturn. Instead, you’d prefer your assets not to be correlated so that if one of them falls, the other one isn’t necessarily falling, too. This statement indicates that, at the time, cryptocurrencies weren’t correlated to stocks and other assets, making them a way to buffer stock market losses or for the stock market to buffer cryptocurrency losses.

However, much has changed in the fast-moving world of cryptocurrencies, including their correlation with the stock market. MoneyGeek’s analysis of cryptocurrency and stock returns found that the correlation between stocks and cryptocurrency has been increasing since 2020.

Increasing correlation to stocks would mean cryptocurrencies writ large are viewed as investment and speculation assets, rather than a traditional currency such as the U.S. dollar or even a traditional store of value, like gold. This shift has implications for how people view and utilize cryptocurrencies in their daily lives and investment portfolios. However, it’s still unclear how the relationship between cryptocurrencies and stocks will evolve over time.

Expert Insights

David Dubofsky, Ph.D., CFA

Book Author at Your Total Wealth

For a person saving for retirement, what is the most you think they should be investing in cryptocurrency?

In our 2020 book, Your Total Wealth, Lyle Sussman and I defined “cryptocurrency” as a “digital asset that can serve as a medium of exchange, i.e., a currency.”

Thus, as assets with some liquidity, many of the thousands of cryptocurrencies can serve as speculative investment vehicles or as a currency for transactions. As assets, individuals can speculate in crypto and hope prices increase. As mediums of exchange, cryptocurrencies are currencies like dollars, yen and euros. Individuals can sometimes buy and sell goods and services, paying for them and getting paid in cryptocurrencies.

Crypto may serve as a store of value. Most investment assets you acquire are paid for in dollars. Some investors may fear that the value of the dollar will erode over time (inflation). In the 1960s and early 1980s, investors invested in gold as a hedge against a declining dollar. With the introduction of cryptocurrencies, investors might invest in cryptocurrencies rather than gold if they are fearful of a collapsing dollar and/or global political and economic uncertainty. Perhaps cryptocurrencies serve the same purpose as gold for these doomsayers.

Crypto has been around for about 15 years, and during that time, I heard repeatedly about the promise that crypto will facilitate commercial transactions. But today, 15 years after it began, the word “promise” remains. Very little transacting has taken place with crypto these past 15 years. And I see very little transacting in the near future. According to Reuters, over $20 billion in transactions in 2023 were illicit. This makes up over 40% of all crypto transactions. Ransomware hackers, rogue states and cybercriminals use crypto for nefarious purposes.

In some countries with very weak currencies, crypto can serve a purpose. Perhaps citizens in those countries should keep their wealth in crypto rather than their own country’s currency. In other countries, using crypto is illegal. But we have yet to see its use for regular transactions take hold anywhere worldwide.

Is cryptocurrency an investment vehicle, or is it something else? How should investors view cryptocurrencies?

As an investment, using standard valuation approaches, bitcoin is overvalued by any standard of what an asset should theoretically be worth. The greater fool theory is driving its recent $70,000 price. As long as the Bitcoin market can attract more players to the party, its price can increase, but fundamentally, it is not worth much, if anything at all. I don’t think the US government will likely allow Bitcoin or any other currently available cryptocurrency to dominate transactions.

If you believe in crypto’s commercial promise and its value to hedge against declines in the value of the dollar, then I’d say that devoting 5% of your portfolio, at most, to cryptocurrencies might make sense. Maybe, at most, another 5% could be invested in stocks that will benefit from future growth in crypto stocks, like Coinbase and MicroStrategy. There are also mutual funds and ETFs that invest in the shares of companies most likely to benefit from the growth in crypto usage. In my humble opinion, committing more than 5–10% of your portfolio to crypto and its associated businesses would be extremely irresponsible and risky. I have nothing invested in crypto. And beware of scammers who pitch cryptocurrency “opportunities” to you.

Methodology

MoneyGeek’s cryptocurrency index was constructed using a market cap weighting of weekly cryptocurrency from April 28, 2013, through February 6, 2022, as reported by CoinMarketCap. Each week, the index is reconstructed to reflect changes in the relative weights of the coins in the index.

We utilized weekly returns of the S&P 500 to reflect stocks; to reflect the return on bonds, the S&P US Aggregate Bond Index was used.

Disclaimer: The information provided on this page is only for educational purposes. MoneyGeek doesn’t recommend that investors buy or sell any particular investments, nor does it offer any financial advisory services.

About Geoff Williams

Geoff Williams has been a personal finance journalist since around the time of the Great Recession of 2008. He’s been writing professionally since the 1990s about a variety of topics, including personal finance, credit cards and loans.

Williams is also the author of several books, including “Washed Away: How the Great Flood of 1913, America’s Most Widespread Natural Disaster, Terrorized a Nation and Changed It Forever” and “C.C. Pyle’s Amazing Foot Race: The True Story of the 1928 Coast-to-Coast Run Across America.”

Born in Columbus, Williams now lives in Loveland, Ohio, with his two teenage daughters.

SOURCES

- BBC. “Bitcoin ‘will recover’ from crash.” Accessed March 18, 2022.

- Chainalysis. “Crypto Crime Trends for 2022: Illicit Transaction Activity Reaches All-Time High in Value, All-Time Low in Share of All Cryptocurrency Activity.” Accessed March 17, 2022.

- CoinMarketCap. “Check Cryptocurrency Price History For The Top Coins | CoinMarketCap.” Accessed February 26, 2022.

- COINTELEGRAPH. “A Dazzling History of Bitcoin’s Ups and Downs.” Accessed March 18, 2022.

- Fortune. “Hackers steal $320 million in crypto from Wormhole DeFi project.” Accessed May 1, 2023.

- National Bureau of Economic Research. “Risks and Returns of Cryptocurrency.” Accessed February 22, 2022.

- S&P Global. “S&P US Aggregate Bond Index | S&P Dow Jones Indices.” Accessed February 26, 2022.

- Worth of Cryptocurrency Market. “CoinGecko.” Accessed February 24, 2022.

- Yahoo Finance. “S&P 500 (^GSPC).” Accessed February 26, 2022.